The State of AI Startups: 2025 Year-End Analysis

An AI Market Watch Special Report

AI is no longer a vertical trend — in 2025 it is the venture market. Across funding rounds, strategic capital flows, enterprise adoption signals, and category dynamics, AI's influence on global innovation has reached a new inflection point.

Drawing on the AI Market Watch database of 2,738 AI startups with VC-grade scoring across six dimensions, along with the latest external data, this analysis dissects where capital is flowing, how value is being created (or concentrated), and what the next phase of the AI boom looks like.

1. A Turning Point: AI Grabs More Than Half of All Venture Capital

In 2025, AI companies captured an unprecedented share of global venture funding — over 50% of total VC dollars raised. According to CB Insights' Q3 2025 report, AI startups accounted for roughly 51% of all global venture funding, a first in recorded trends.

This is not trivial — it signals a paradigm shift in how capital allocators perceive technology risk and reward. Where in prior decades, leadership in basic software, mobile, or cloud were the key fund flows, AI now vies with total software as the predominant investment theme.

Key dynamics include:

Despite an overall decline in deal volume, total funding has remained above $45B per quarter for multiple quarters.

AI funding is more top-heavy and concentrated than ever — with the largest rounds skewing aggregate totals.

PitchBook data from H1 2025 places AI at ~53% of global VC funding, and up to 64% in the U.S.

Insight: When more than half of all venture capital goes to a single theme, it's not just investor preference — it reflects structural shifts in technology, enterprise adoption, and competitive advantage.

2. Capital Concentration: Mega Rounds, Corporate Capital, and Winner-Take-Most Dynamics

2025 is the year of mega-deals and strategic capital:

Foundation Model Leaders:

OpenAI reached a $500B valuation in October secondary sales, with revenue on track for $13.5B in 2025 and IPO discussions intensifying for H2 2026.

Anthropic hit a $183B valuation in September 2025 after raising $13B Series F (led by Iconiq, Fidelity, Lightspeed), later reaching $350B following Microsoft and Nvidia's combined $15B investment in November 2025. Revenue exploded from $1B to $5.5B+ run-rate in just 10 months.

Infrastructure, Compute and Data:

Nvidia's acquisition of Groq for $20B (December 2025) — Nvidia's largest deal ever — signals aggressive consolidation in AI inference infrastructure.

Unconventional AI raised a stunning $475M seed round at $4.5B valuation (December 2025), founded just two months prior by former Databricks AI head Naveen Rao. Backed by a16z, Lightspeed, and Jeff Bezos.

Databricks raised a $4B+ Series L at a $134B valuation (December 2025), with revenue at $4.8B run-rate.

This capital has not just come from traditional VC — corporate venture arms and private equity are increasingly dominant, particularly as strategic players seek control of future AI infrastructure and platforms.

Insight: This kind of capital concentration has three implications:

Liquidity pressure on smaller startups — less capital for early stage progress without clear differentiation.

Extended runway for category leaders, especially infrastructure and foundational models.

A bifurcated market: a handful of hyper-funded platforms vs. a long tail of specialized, lean AI builders.

3. AI Market Watch Database: A Unique View into the AI Startup Landscape

Our proprietary database of 2,738 AI startups provides granular insights unavailable from aggregated market reports. Key findings:

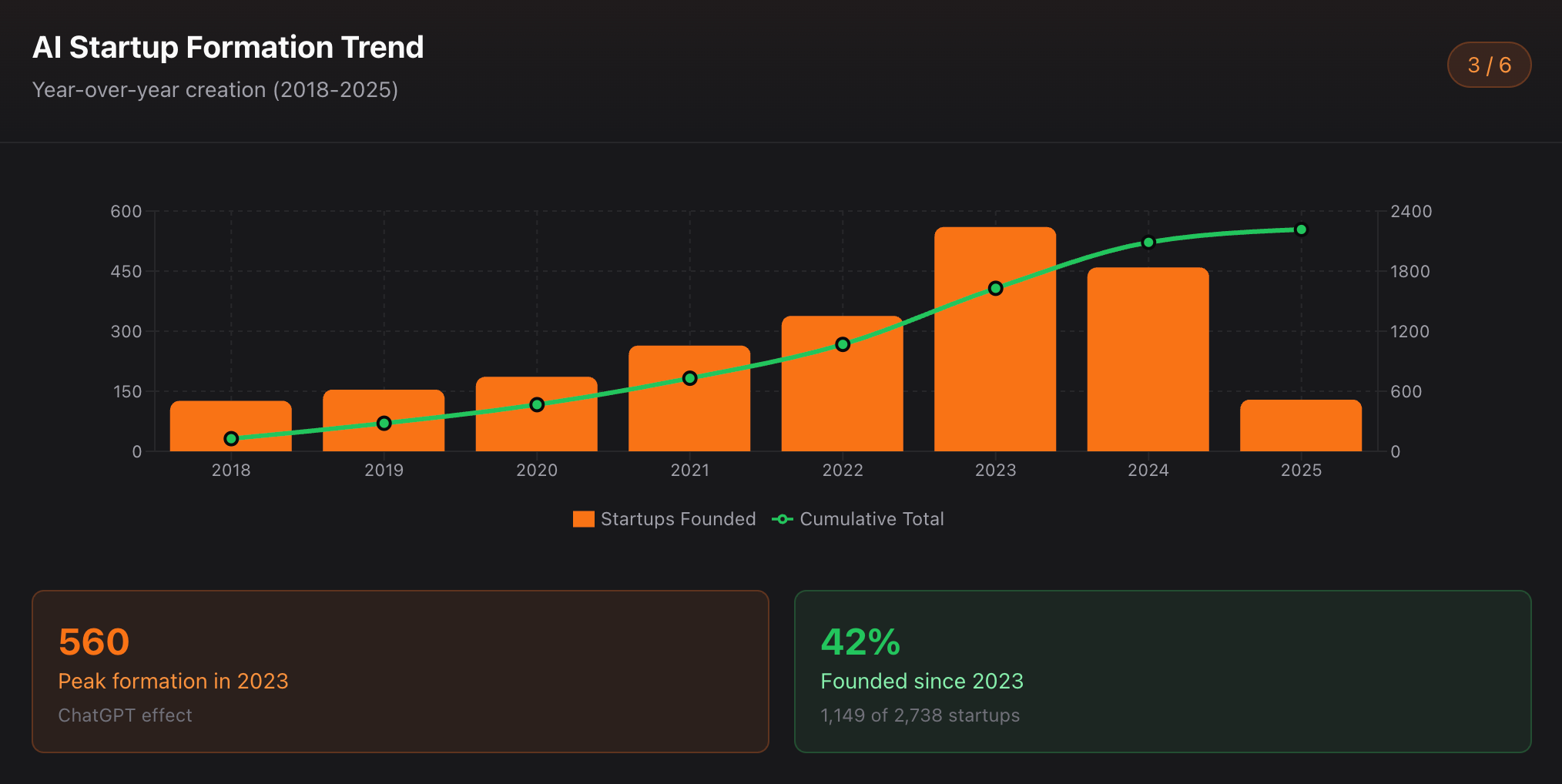

Startup Formation Trends

Metric | Count |

|---|---|

Total startups tracked | 2,738 |

Founded 2023 or later | 1,149 (42%) |

Founded 2024 or later | 589 (21.5%) |

Companies with VC scores | 2,738 (100%) |

The surge in AI startup formation is remarkable: 42% of all AI startups in our database were founded in the last two years, indicating an unprecedented wave of entrepreneurial activity in the AI space.

Year-over-Year Formation

Year | Startups Founded |

|---|---|

2018 | 126 |

2019 | 154 |

2020 | 186 |

2021 | 264 |

2022 | 338 |

2023 | 560 |

2024 | 459 |

2025 (YTD) | 129 |

The 2023 peak reflects the ChatGPT-catalyzed wave of AI entrepreneurship, with formation rates remaining elevated but moderating in 2024-2025 as the market matures.

Important Note: Our database tracks AI startups that have achieved some level of traction and visibility — typically those with initial funding, product launches, or media coverage. The actual number of AI companies founded in 2024-2025 is likely significantly higher, as many early-stage ventures have yet to surface in our data collection. This survivor bias means our 2023 peak may actually represent the cohort that has successfully emerged from stealth or secured early funding, rather than peak formation year.

4. Category Analysis: Where Innovation is Happening

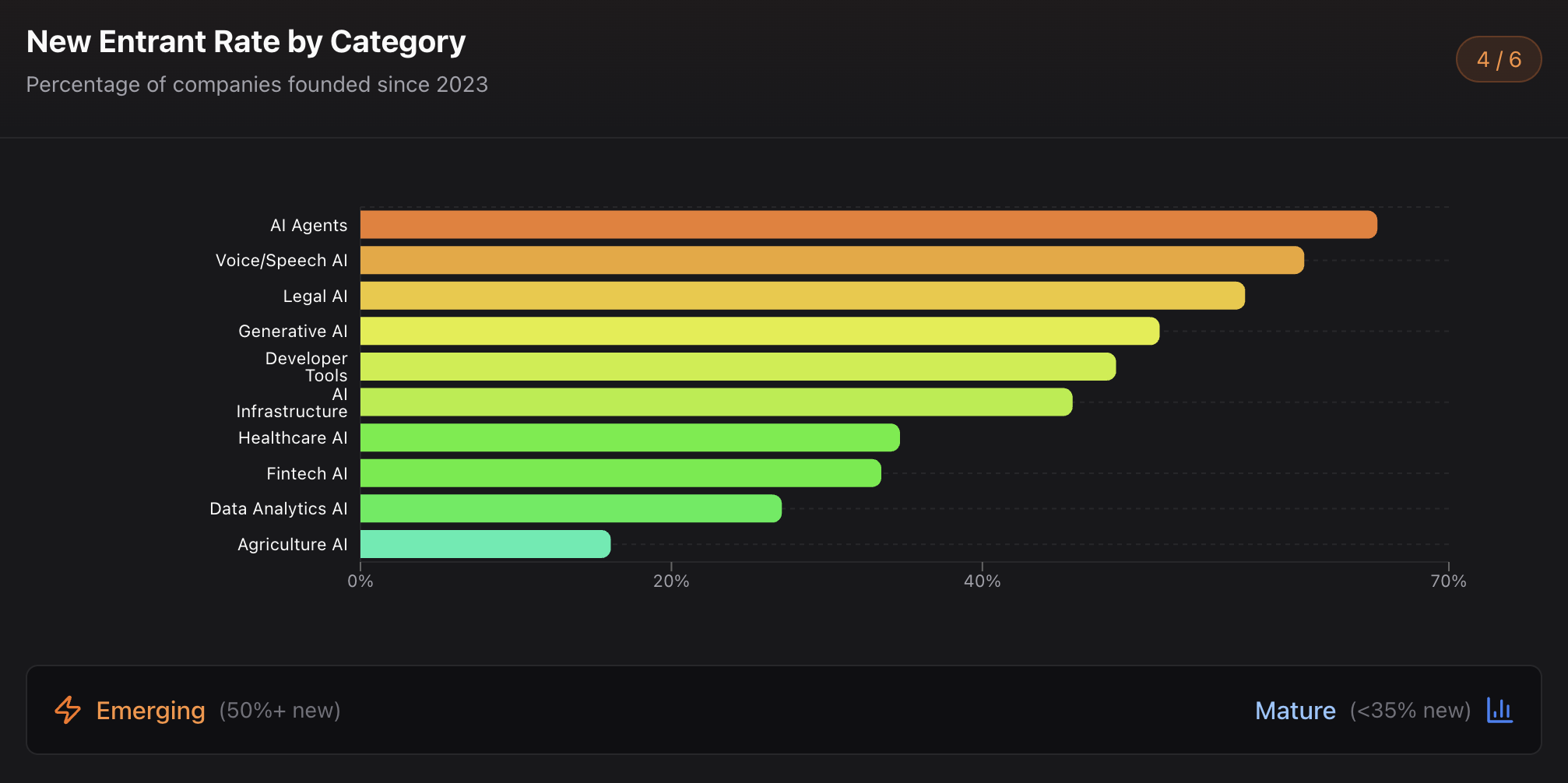

Hottest Categories (High New Entrant Rates, 2023+)

Our data reveals which AI categories are attracting the most new founders:

Category | Total | New Entrants (2023+) | % New |

|---|---|---|---|

AI Agents | 208 | 136 | 65.4% |

Voice/Speech AI | 56 | 34 | 60.7% |

Legal AI | 58 | 33 | 56.9% |

Generative AI | 138 | 71 | 51.4% |

Developer Tools | 111 | 54 | 48.6% |

Sales & Marketing AI | 171 | 83 | 48.5% |

AI Infrastructure | 277 | 127 | 45.8% |

AI Agents lead with 65.4% new entrants — nearly two-thirds of all AI Agent companies in our database were founded since 2023, confirming this as the hottest emerging category.

Recent Examples (December 2025):

Resolve AI (SRE automation) hit $1B valuation with Series A led by Lightspeed, founded by ex-Splunk executives

Aaru (AI synthetic research) reached $1B headline valuation with Series A led by Redpoint — founded March 2024, already serving Accenture, EY, and political campaigns

Mature & Pre-Expansion Categories (Lower New Entrant Rates)

Category | Total | New Entrants (2023+) | % New | Interpretation |

|---|---|---|---|---|

Healthcare AI | 265 | 92 | 34.7% | Mature market, high regulatory barriers |

Fintech AI | 251 | 84 | 33.5% | Established players, compliance complexity |

Data Analytics AI | 85 | 23 | 27.1% | Mature, absorbed into larger platforms |

Logistics/Supply Chain AI | 70 | 18 | 25.7% | Enterprise-dominated, long sales cycles |

AI in Agriculture | 31 | 5 | 16.1% | Pre-expansion: infrastructure gaps limit scaling |

Lower new entrant rates indicate either mature markets with established players and higher barriers to entry, OR pre-expansion categories where enabling infrastructure (connectivity, data availability, distribution channels) hasn't yet reached the threshold for mass startup formation.

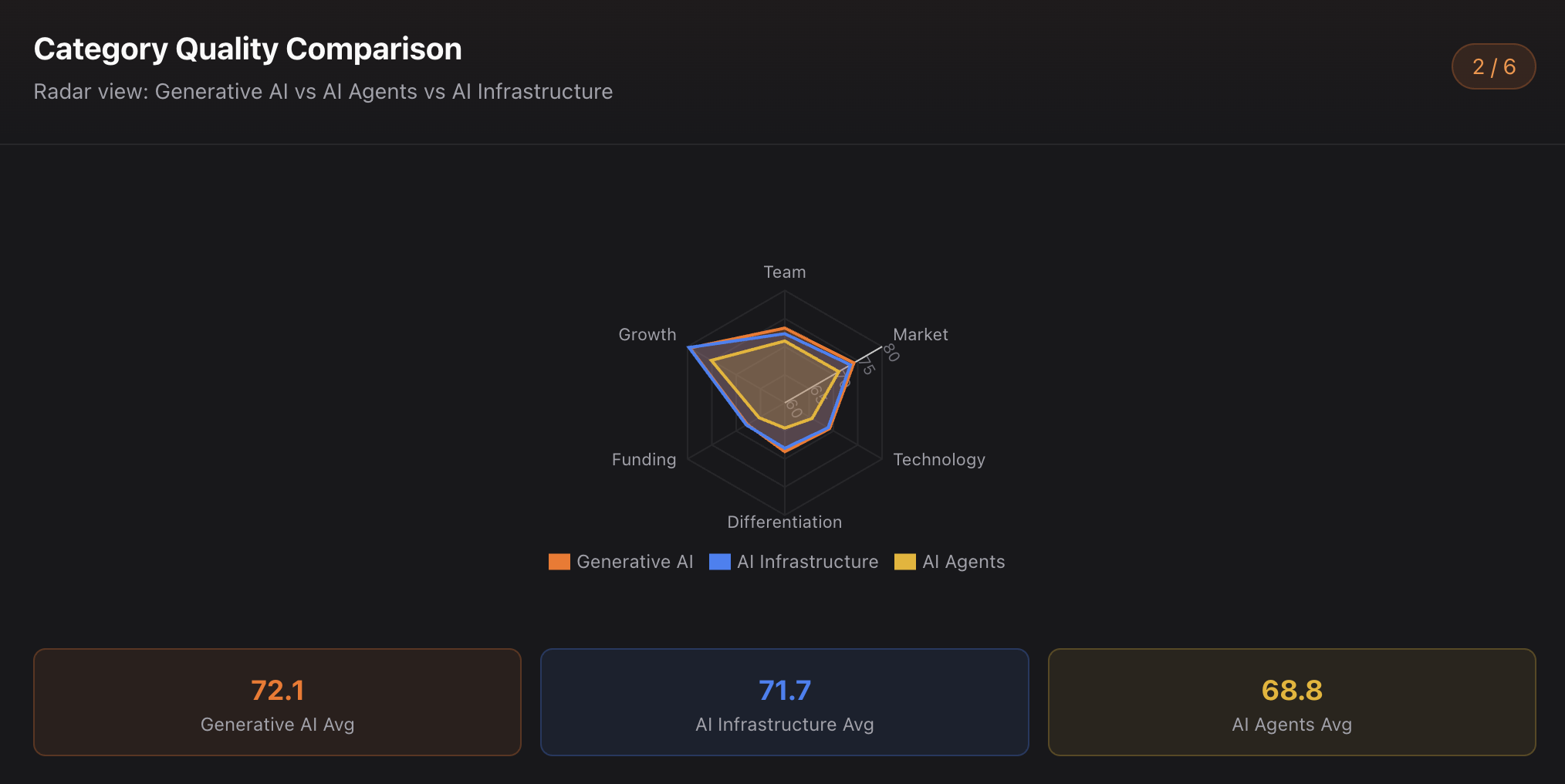

5. VC Score Analysis: Category Quality Benchmarks

Our proprietary VC scoring evaluates startups across six dimensions (Team, Market, Technology, Differentiation, Funding, Growth). Here's how categories compare:

Category Performance by VC Score Dimension

Category | Team | Market | Tech | Diff | Funding | Growth | Avg |

|---|---|---|---|---|---|---|---|

Generative AI | 73.3 | 74.2 | 69.2 | 68.7 | 67.7 | 79.5 | 72.1 |

AI Infrastructure | 72.3 | 73.5 | 68.9 | 68.1 | 67.9 | 79.7 | 71.7 |

Cybersecurity AI | 72.3 | 73.4 | 69.3 | 68.1 | 66.7 | 78.4 | 71.4 |

Healthcare AI | 72.2 | 72.0 | 68.6 | 67.6 | 65.9 | 78.8 | 70.9 |

Developer Tools | 72.7 | 72.6 | 67.6 | 67.2 | 67.6 | 77.6 | 70.9 |

AI Agents | 71.0 | 71.1 | 65.6 | 64.5 | 65.3 | 75.1 | 68.8 |

Key Finding: The AI Agents Paradox

AI Agents show the highest new entrant rate (65.4%) but the lowest average scores (68.8) across most dimensions. This reflects:

Early-stage concentration: Most AI Agent companies are pre-Series A with limited funding history

Unproven execution: High formation rate means many untested teams

Differentiation challenge: Crowded space makes standing out difficult (lowest differentiation score at 64.5 — a 6.5-point gap from the mean)

Yet the leading AI Agent companies are achieving remarkable success:

Sierra (Bret Taylor's customer service AI) raised $350M at $10B valuation (September 2025), with ARR exceeding $100M

Cognition (Devin AI coding agent) raised $400M at $10.2B valuation (September 2025), with ARR jumping from $1M to $73M in just 9 months

Insight for Investors: AI Agents represent high-risk/high-reward opportunities. The category's low average scores mask significant variance — top-quartile AI Agent companies are achieving exceptional outcomes, while the long tail dilutes averages. The gap between winners and the rest is widening.

6. Regional Dynamics: India's Rise

While the U.S. remains the dominant AI hub (representing 56% of our database), India has emerged as the clear #2 ecosystem with 225 AI startups tracked.

India's growth trajectory is notable: strong English-language technical talent, favorable cost structures, and increasing domestic enterprise adoption are driving formation. The emergence of India-based AI unicorns and significant government initiatives (India AI Mission) suggest this trend will accelerate.

Data Note: Our database relies primarily on English-language sources, which may undercount AI activity in non-English markets such as China, Japan, and South Korea. Regional ecosystem analyses should be interpreted with this limitation in mind.

7. The Series A Bottleneck: A Critical Chokepoint

Analysis of funding stage distribution reveals a significant funnel pinch:

Stage | Count | Founded 2023+ |

|---|---|---|

Pre-Seed | 53 | 49 (92.5%) |

Seed Stage | 136 | 90 (66.2%) |

Series A | 57 | 19 (33.3%) |

Series B | 24 | 0 (0%) |

Growth Stage | 34 | 1 (2.9%) |

Key Observation: 92.5% of Pre-Seed companies and 66.2% of Seed companies were founded since 2023, but only 33.3% of Series A companies. Zero Series B companies in our database were founded since 2023.

This pattern is visible even in the most successful cohorts. Consider the contrast:

Unconventional AI (founded October 2025) raised $475M seed at $4.5B valuation — exceptional capital access for proven founders

Meanwhile, the vast majority of 2023-2024 seed-stage companies have yet to close Series A rounds

Insight: The "graduation rate" from Seed to Series A is becoming increasingly selective. Despite the surge in seed-stage formation, fewer startups are successfully transitioning to growth stages. Combined with capital concentration at the top, this creates a funnel pinch where investors are highly selective and founder pedigree matters more than ever.

8. Enterprise AI: Adoption Has Plateaued but Deepened in Functionality

According to McKinsey's 2025 enterprise AI survey:

88% of organizations now use AI in at least one function, up from 78% last year.

However, usage is not uniform:

Many companies still struggle to scale beyond point solutions.

Strategic AI spend is concentrated in product leaders and early adopters, with others trailing in deployments.

This aligns with trends showing enterprise AI budgets growing but not evenly:

Menlo Ventures data indicates that generative AI spend jumped to $37B in 2025, a 3x increase from 2024.

Enterprise AI Agent Adoption Milestones (2025):

Sierra's agents now reach over 50% of U.S. families through healthcare and financial services deployments

Cognition's Devin powers engineering teams at Goldman Sachs, Citi, Dell, Cisco, Ramp, Palantir, and Nubank

G2's 2025 survey finds ~57% of companies have AI agents in production, not just in pilot

Insight: AI is pervasive, but its depth varies — from pilot programs to deep, automated workflows. The next frontier is scalable, measurable ROI, not just experimentation.

9. AI Agents: From Hype to Production Deployment

Among AI categories, AI agents stand out not just in VC momentum but in actual adoption and deployment.

Our database confirms:

AI Agents category has 65.4% new entrants (highest of any category)

208 companies tracked, making it a top-5 category by size

Rapid formation despite lower average VC scores indicates market timing advantage

Production Deployment Evidence (2025):

Company | Revenue Milestone | Enterprise Deployments |

|---|---|---|

Salesforce Agentforce | $540M ARR, 18,500 customers, 3B workflows/month | Adecco automates 30-step recruiting; Engine cuts handle time 15%; 1-800-Accountant resolves 70% of chats autonomously |

Sierra | $100M ARR in 21 months, $10B valuation | Discord, Rivian, SoFi, ADT, Cigna — agents handle patient authentication, mortgage origination, credit card replacements |

Moveworks | $100M ARR, acquired by ServiceNow for $2.85B | 350+ enterprises, 10% of Fortune 500; IT/HR ticket automation at Procore saves 4,000 operator hours/quarter |

Glean | $100M+ ARR, $7.2B valuation | Databricks, Booking.com, Duolingo — autonomous agents with enterprise memory across 100+ integrations |

Emerging Players: Cognition ($10.2B valuation, $73M→$155M ARR), Writer ($1.9B), and vertical-specific agents like Resolve AI (SRE automation) and Aaru (synthetic research) signal continued category expansion.

Market Projections:

AI agents sector estimated at ~$7.3B–$7.9B in 2025, with 40%+ CAGR

Salesforce reports AI agent usage up 233% in six months (Slack Workforce Index)

G2's 2025 survey finds ~57% of companies have AI agents in production, not just in pilot

Insight: What was once considered "experimental automation" has crossed the production threshold. The 2025 wave of $100M+ ARR milestones — achieved in under two years by multiple players — confirms AI agents are no longer pilot projects but operational infrastructure. However, the gap between leaders and the long tail remains significant: while top-tier companies deploy agents at enterprise scale, the category's low average VC scores (Section 5) reflect that most startups have yet to prove production readiness.

10. What 2026 Looks Like: Opportunities & Cautions

2025 data suggests both opportunity and constraint:

Bullish Signals

Continued dominance of AI in venture flows (50%+ of all VC)

Rapid growth of autonomous and embedded AI tools

Strategic expansion by cloud, compute, and data ecosystem players

42% of AI startups founded in last 2 years indicates sustained innovation

AI Agent companies achieving $10B+ valuations within 18-24 months of founding

Emerging Cautions

Capital concentration ▲ — Top 5 AI companies absorbing disproportionate funding

Series A bottleneck — High seed formation, zero Series B companies founded since 2023

Category crowding — AI Agents show lowest differentiation scores despite highest formation

Consolidation accelerating — Nvidia's $20B Groq acquisition signals infrastructure rollup

Tech risk and governance complexity rising fast

Insight for the Ecosystem

To succeed beyond headline capital numbers, teams must deliver:

Real business outcomes — not just technical novelty

Go-to-market traction — proven customer acquisition

Robust governance — especially for agentic use cases

Clear differentiation — in a market where 65% of AI Agent companies are less than 2 years old

Founder pedigree — increasingly important for breaking through Series A bottleneck

Methodology Note

This report combines:

AI Market Watch proprietary database: 2,738 AI startups with VC-grade scoring across Team, Market, Technology, Differentiation, Funding, and Growth dimensions

External sources: CB Insights, PitchBook, McKinsey, Menlo Ventures, G2, PwC, TechCrunch, Bloomberg, and company announcements

Analysis period: Data as of December 2025

Database Limitations:

English-language source bias may undercount non-English market activity

Tracked startups have achieved some visibility (funding, product launch, media coverage)

2024-2025 formation numbers likely understate actual startup creation due to lag in data capture

Conclusion: From Trend to Foundation

2025 marks a watershed:

AI is no longer an experimental frontier — it is the core engine of venture capital, strategic investment, and enterprise technology transformation.

Where capital once flows toward promise, it now flows toward proven execution, enterprise integration, and scalable platform plays. The future of AI investment will be shaped by both bold foundational bets and disciplined growth strategies.

Our database of 2,738 startups — with 42% founded since 2023 — represents the largest wave of AI entrepreneurship in history. The December 2025 funding events demonstrate both the extraordinary opportunity (Unconventional AI's $475M seed) and intensifying consolidation (Nvidia-Groq) that will define the next chapter.

The companies that emerge from this wave will define the next decade of technology.