TESOLLO, a South Korean developer of multi-joint robotic hands, has closed a Series B round and form...

The AMW Read

Incremental funding and IPO start for a known robotics hardware player; significance is sub-segment (robotic hands) within the broader Robotics/Physical AI segment.

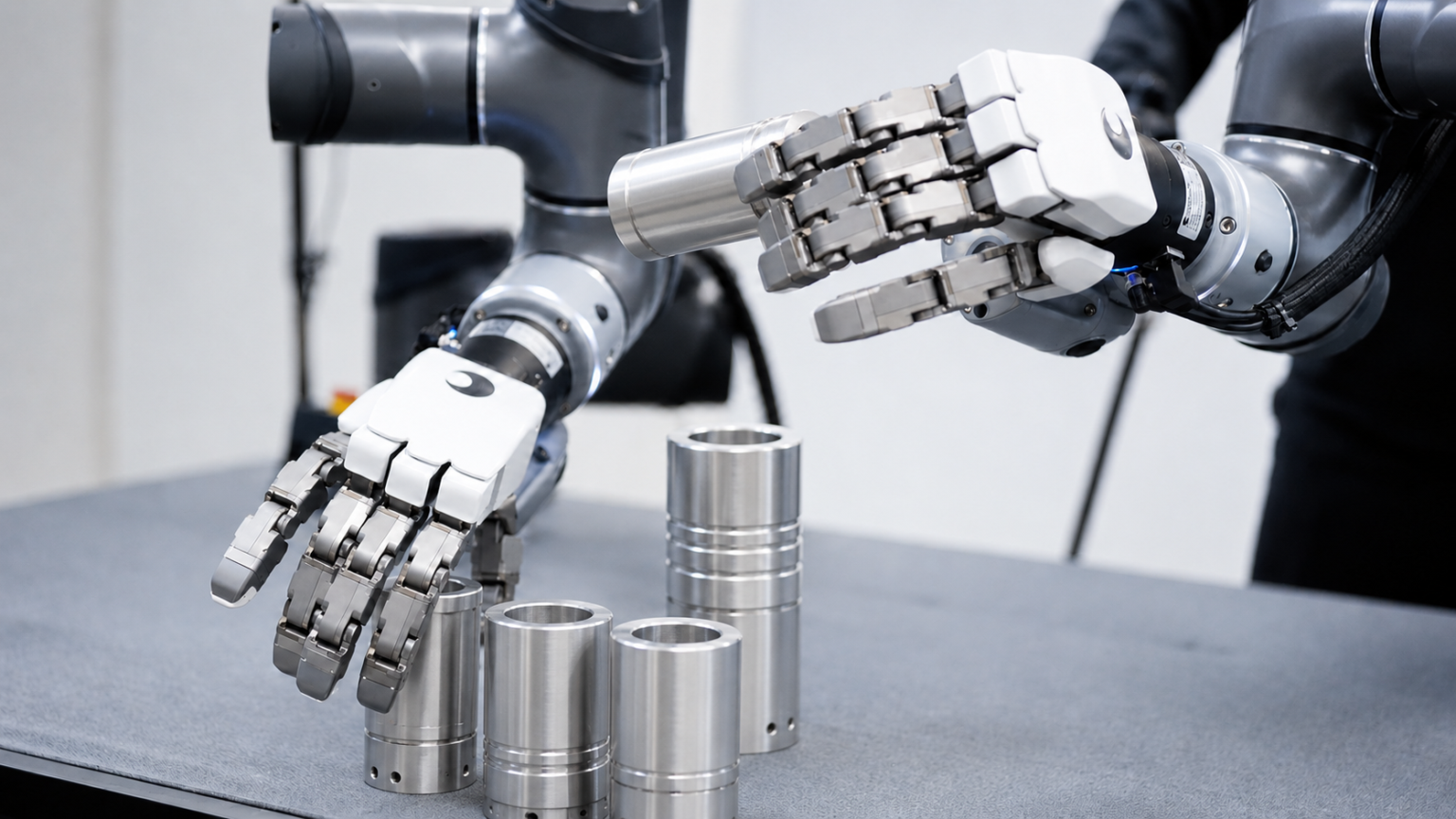

TESOLLO, a South Korean developer of multi-joint robotic hands, has closed a Series B round and formally launched its IPO process with KB Securities as lead underwriter, targeting a listing on Korea's technology-exception track by 2027 or later. The Series B saw participation from existing backers POSCO Investment, KB Investment, and Enlight Ventures, alongside new strategic investors Daesung Hitech and HL Mando. The company commercializes its Delto Gripper line, which includes humanoid robotic hands and multi-joint grippers powered by proprietary actuators and AI-driven dexterity systems. TESOLLO exports to 19 countries including the US, China, and Japan, with overseas sales now exceeding domestic revenue.

Why it matters: This event extends the capital-compression arc visible in robotics hardware, where specialized gripper and end-effector companies command premium valuations amid the humanoid robotics build-out. TESOLLO sits at the intersection of industrial automation (bearing rich enterprise margins) and the speculative humanoid mass-production wave, a dual-market strategy that de-risks its growth timeline. The IPO timeline (2027+) suggests the company expects sustained revenue scaling before public market entry, a pattern reminiscent of the serial funding strategy seen in other hardware-heavy physical AI players. The strategic investor mix—industrial conglomerates alongside venture arms—indicates supply-chain integration ambitions, a recurring moat-building move in robotics hardware.

Grounded expert take: While TESOLLO's proprietary actuator technology and 19-country export base provide tangible differentiation, the company's true test is mass-production readiness. The humanoid market remains nascent, and TESOLLO's success will depend on whether it can achieve cost curves that underpin volume deployment. The IPO selection of a technology-exception track—typically for high-growth tech firms—signals confidence in sustained R&D spending. However, the 2027 horizon leaves ample room for competitive pressure from both incumbent industrial automation giants and emerging humanoid-native players. Investors should watch for gross margin trends and manufacturing scale milestones as leading indicators.