Executive Summary

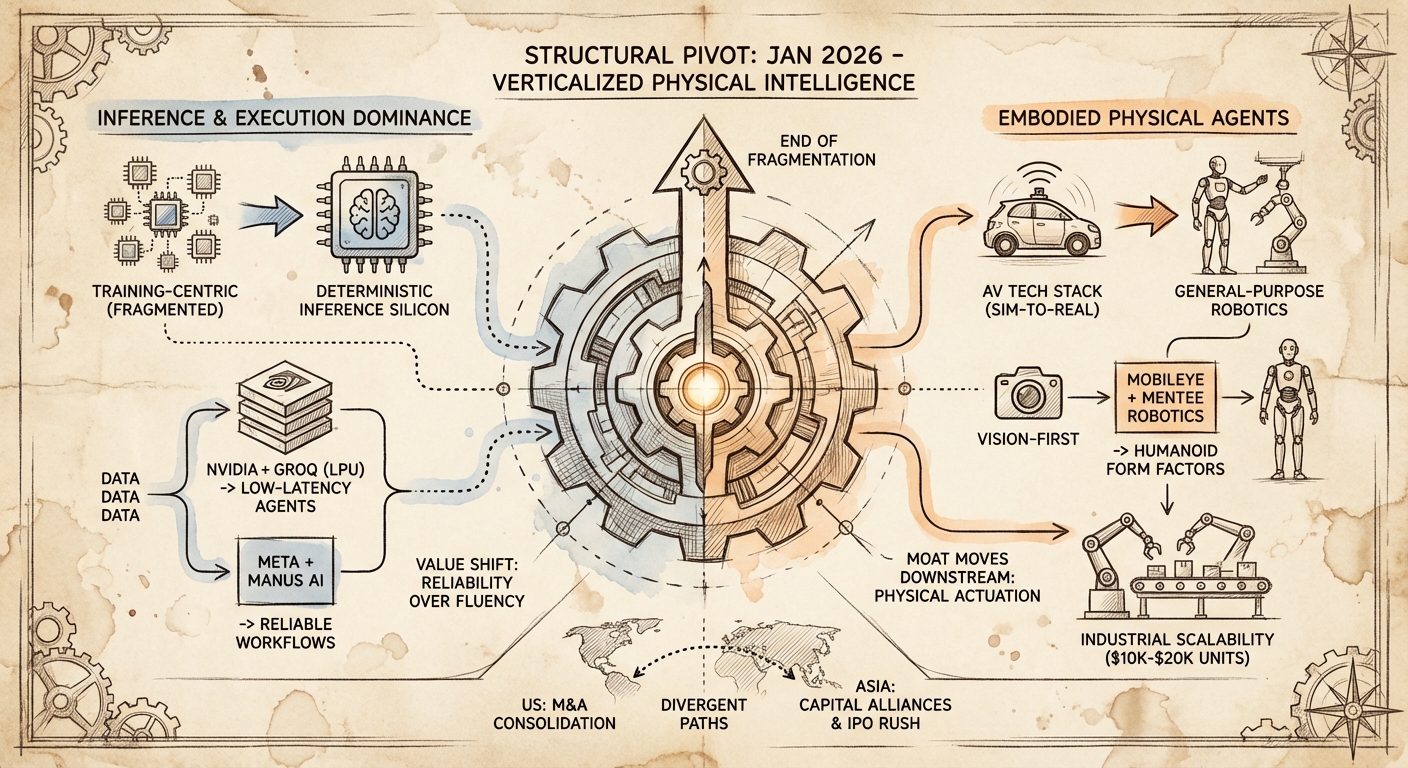

The first two weeks of 2026 have delivered a decisive market signal: the era of fragmented experimentation is yielding to structural consolidation. Two mega-cap transactions - Nvidia’s $20 billion acquisition of Groq assets and Mobileye’s $900 million purchase of Mentee Robotics - indicate a fundamental shift in the industry’s value capture mechanisms.

We are witnessing a transition from training-centric capital allocation to inference and execution dominance. Infrastructure leaders are no longer content supplying components; they are aggressively moving to own the entire operational stack, from deterministic inference silicon to embodied physical agents. This analysis dissects the economic and technical drivers behind this consolidation and contrasts Western M&A strategies with the capital alliance models emerging in Asian markets.

The Market Signal

Two distinct but parallel consolidation events define the current market landscape:

Nvidia Consolidates the Inference Layer: The $20 billion cash acquisition of Groq assets represents a defensive and offensive maneuver. By absorbing Groq’s Language Processing Unit (LPU) architecture, Nvidia effectively neutralizes its most capable rival in low-latency inference while solving the memory-bandwidth bottleneck that plagues traditional GPU architectures during real-time token generation.

Mobileye Pivots to Embodied AI: The $900 million acquisition of Mentee Robotics signals that the autonomous vehicle (AV) technology stack is being repurposed for general-purpose robotics. Mobileye is validating the thesis that self-driving cars were simply the first instance of embodied AI, and that the same computer vision and path-planning architectures can scale to humanoid form factors.

Collectively, these moves suggest that the "moat" is moving downstream - from having the biggest model to having the most efficient runtime environment and the most capable physical actuation.

Technical and Strategic Deep Dive

1. The Deterministic Compute Shift

Nvidia’s strategic absorption of Groq addresses a critical architectural limitation in the deployment of agentic AI: non-deterministic latency. Groq’s architecture, which relies on massive amounts of SRAM rather than High Bandwidth Memory (HBM), bypasses the "memory wall" - the bottleneck where data transfer speeds lag behind processing speeds.

For agentic workflows that require sequential reasoning steps (Chain-of-Thought), latency is compounding. By integrating Groq’s LPU technology, Nvidia is positioning its hardware stack to dominate not just high-throughput training, but the real-time, low-latency inference required for complex, multi-step AI agents. This effectively raises the barrier to entry for alternative chipmakers focusing solely on raw FLOPs.

2. The Convergence of AV and Robotics

Mobileye’s acquisition illustrates the "Sim-to-Real" capital efficiency. Training robotic foundation models from scratch is prohibitively expensive due to the scarcity of real-world physical data. However, Mobileye’s vast repository of driving video data and edge-case scenarios provides a pre-validated training ground for spatial awareness.

Mentee Robotics utilizes a "vision-first" approach, aligning perfectly with Mobileye’s camera-centric methodology (shunning LiDAR). This integration suggests that future humanoid development will likely be driven by automotive tier-ones diversifying into industrial labor, leveraging their existing manufacturing scale and safety-critical software certification processes.

3. The Agentic Execution Layer

Complementing the hardware shifts, Meta’s completed $2 billion acquisition of Manus AI (despite regulatory friction) underscores the value of the execution layer. Manus distinguishes itself not by model size, but by its ability to execute long-horizon tasks (consuming up to 100,000 tokens per workflow). This signals that the market now values reliability of outcome over conversational fluency. The bottleneck for enterprise adoption is no longer generating text; it is trusting an agent to complete a multi-step workflow without hallucinating or stalling.

Contextual Synthesis: Divergent Global Strategies

While US firms leverage balance sheets for M&A, the Asian market is responding through capital alliances and rapid public listings to secure liquidity for hardware sovereignty.

China’s "Triple Giant" Alliance: In a rare move, fierce rivals ByteDance, Alibaba, and Meituan jointly backed X Square Robot in a $143 million Series A++ round. This suggests a state-coordinated or market-forced mandate to accelerate domestic embodied AI capabilities without relying on Western hardware integration.

The IPO Rush: The Hong Kong listings of Biren Technology, Zhipu AI, and MiniMax in early January (raising over $1.8 billion combined) demonstrate a rush to secure public capital. Unlike Western firms consolidating under tech giants, Chinese champions are seeking independence via public markets to fund the immense R&D costs required to build sovereign chip and model stacks.

Future Outlook

The consolidation of January 2026 sets a precedent for the remainder of the year. We anticipate:

The Squeeze on Mid-Tier Hardware: As Nvidia integrates LPU tech, specialized inference chip startups will face existential pressure to demonstrate superior TCO (Total Cost of Ownership) or be acquired.

Industrialization of Humanoids: With automotive players like Mobileye entering the fray, we expect the focus in robotics to shift from "dexterity demos" to "manufacturing scalability." The race is now about who can produce reliable units at the $10,000–$20,000 price point.

Agentic Clouds: Cloud providers (hyperscalers) will increasingly offer "Token-as-a-Service" optimized for specific agentic behaviors (reasoning, coding, planning), moving away from generic model hosting.

For investors and founders, the signal is clear: value is accruing to those who control the physical manifestation of AI (chips, robots) and the reliable execution of its outputs.