Google will pay SpaceX $920 million per month for compute capacity starting in October 2026, a deal disclosed in a SpaceX regulatory filing (https://techcrunch.com/2026/06/05/google-will-pay-spacex-920m-per-month-for-compute/). That single number — nearly $1 billion a month for rent on someone else's GPUs — is the cleanest signal yet that the structural shift from training-centric to inference-optimized infrastructure is not theoretical: it is happening in real time, at the largest possible scale, and it is re-architecting how capital, silicon, and deployment velocity are organized across the AI stack.

The old model treated inference as an afterthought to training. Build a giant cluster, train a model, then serve tokens on whatever capacity is left over. That model is breaking because inference demand is exploding faster than any single company's internal buildout can absorb. Fireworks AI, the inference platform founded by former Meta AI lead Lin Qiao, is in discussions for a new funding round at an approximately $15 billion valuation (https://eu.36kr.com/zh/p/3831510606473090). The company now processes roughly 30 trillion tokens per day and reached $315 million in annualized revenue by February 2026, up 416% year-over-year (https://eu.36kr.com/zh/p/3831510606473090). Its customers include Cursor, Uber, Samsung, Notion, and Shopify — a mix of enterprise and developer segments where enterprise appears to be the larger monetization channel (https://getlatka.com/companies/fireworks.ai). Fireworks AI's trajectory from zero revenue four years ago to this scale challenges the notion that only vertically integrated lab-to-application players can achieve escape velocity in AI monetization. It also updates the open debate about whether inference infrastructure can generate venture-scale returns: the $15 billion target valuation — up from $5.52 billion in the B round — suggests the market now believes the "token toll road" thesis can sustain hyperscaler-level margins (https://eu.36kr.com/zh/p/3831510606473090).

The capital flows behind this shift are staggering in their velocity and concentration. SoftBank Group announced plans to invest up to €75 billion (~$87 billion) to build 5 gigawatts of data center capacity in France, making it the company's largest AI infrastructure investment in Europe (https://techcrunch.com/2026/05/30/softbank-says-it-will-invest-up-to-e75-billion-to-build-french-data-centers/). AirTrunk, the Blackstone-backed data center operator, committed $30 billion for 5 gigawatts of AI data centers in India by 2030 (https://techcrunch.com/2026/06/05/airtrunk-commits-30b-to-build-5gw-of-ai-data-centers-in-india/). Helion, a nuclear fusion startup, raised $465 million at a $15.5 billion valuation, nearly tripling from $5.4 billion in January 2025, driven by AI data-center power demand (https://www.mining.com/web/nuclear-startup-helion-hits-15-5-billion-valuation-in-latest-funding-round/). Supabase, a backend-as-a-service platform for AI application development, raised a $500 million Series F at a $10 billion pre-money valuation, doubling from October 2025 (https://www.techmeme.com/260604/p41). These are not round-number coincidences. They represent a compression of capital into infrastructure assets that can serve inference demand at scale, and investors are pricing them at premiums once reserved for foundation-model labs.

The most vivid example of the velocity thesis comes from Meta, which has constructed six weatherproof tents outside New Albany, Ohio, to house multi-gigawatt AI data centers (https://techcrunch.com/2026/06/04/meta-steals-a-tactic-from-tesla-and-builds-data-centers-in-tents/). The 125,000-square-foot tents, built between April and June 2026, host billions of dollars in AI chips and draw 200 megawatts from modular gas turbines. Meta has signaled up to $145 billion in total capital expenditure, and its stock is down 5% year-to-date (https://techcrunch.com/2026/06/04/meta-steals-a-tactic-from-tesla-and-builds-data-centers-in-tents/). The strategy borrows directly from Tesla's 2018 Model 3 production tents in Fremont, and it reflects a fundamental re-engineering of the physical plant of AI compute: swapping permanent data center construction cycles of 2-3 years for deployable structures that can be operational in months. The pattern echoes the CoreWeave case study from the internal frame — where a commodity-finance team treated GPUs as depreciable long-duration assets collateralizing debt — but Meta is now applying a similar logic to the building itself. The tent strategy resolves an open debate about whether hyperscaler infrastructure can keep pace with model-release cadence. Meta's own delay in shipping its Muse Spark developer API suggests the bottleneck is not just model readiness but physical capacity to serve inference at scale (https://techcrunch.com/2026/06/04/meta-steals-a-tactic-from-tesla-and-builds-data-centers-in-tents/).

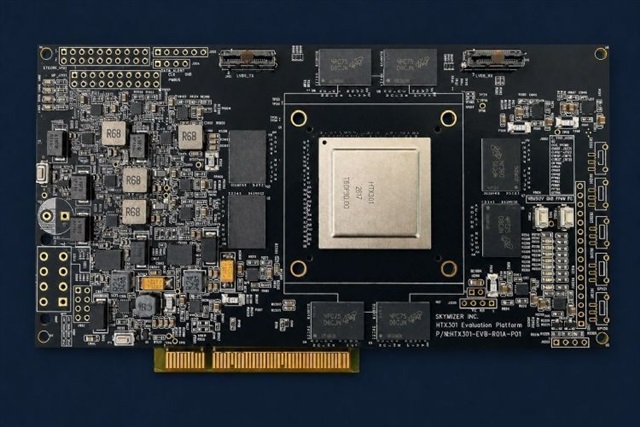

The silicon layer is also re-architecting for inference. Intel disclosed plans for a data center GPU codenamed Crescent Island, built on Xe3P architecture and designed specifically for AI inference workloads (https://startupfortune.com/intel-is-preparing-a-new-ai-chip-to-challenge-nvidia-this-year/). Customer sampling is expected in the second half of 2026. The chip uses LPDDR5X memory — up to 480GB in partner designs — rather than the high-bandwidth memory used in Nvidia's top-tier accelerators (https://wccftech.com/intel-crescent-island-xe3p-gpu-packs-480-gb-of-cost-optimized-lpddr5x-memory/). The bandwidth comparison is stark: Crescent Island's memory bandwidth is estimated at roughly 684 GB/s to 1.5 TB/s depending on configuration, while Nvidia's H200-class HBM3e delivers 4.8 TB/s (https://wccftech.com/intel-crescent-island-xe3p-gpu-packs-480-gb-of-cost-optimized-lpddr5x-memory/). Intel is betting that for cost-sensitive, KV-cache-heavy inference deployments, capacity matters more than peak bandwidth — a bet that becomes more credible as model context windows expand into the millions of tokens. Qualcomm made a parallel move at COMPUTEX 2026, unveiling "Dragonfly," a new product brand for data center AI infrastructure (https://ascii.jp/elem/000/004/407/4407245/). CEO Cristiano Amon declared 2026 "the year of the agent" and projected global token demand reaching 401.48 quintillion by 2030, arguing that agentic AI would shift compute demand from device-only to a distributed cloud-edge model (https://ascii.jp/elem/000/004/407/4407245/). Skymizer launched the HTX301, a decode-first accelerator chip for on-premises large-model inference, at COMPUTEX 2026 (https://www.digitimes.com/news/a20260601PD201/skymizer-accelerator-gpu-taiwan-2026.html). XCENA raised a $135 million Series B at a $570 million valuation for its MX1 chip, which processes AI data directly within memory via the CXL interface (https://theaiinsider.tech/2026/06/02/xcena-announces-135m-to-put-ai-compute-inside-memory-chips-and-cut-infrastructure-costs/). Each of these silicon plays targets a different bottleneck — memory bandwidth, power efficiency, on-premises security, or KV cache management — but they share a common thesis: the training-centric GPU oligopoly is not optimized for the inference workload that now dominates compute demand.

The counter-signal is that Nvidia is not standing still. At GTC Taipei, NVIDIA launched the DGX Station for Windows, a desktop AI supercomputer powered by the GB300 Grace Blackwell Ultra Desktop Superchip, delivering up to 20 petaflops of FP4 performance and 748 GB of coherent memory (https://ascii.jp/elem/000/004/407/4407314/). This brings Blackwell-class compute to a desk-side form factor with built-in agent isolation and fleet management, extending the hyperscaler distribution moat into the enterprise desktop. The real test for Intel's Crescent Island, Qualcomm's Dragonfly, and Skymizer's HTX301 is whether they can overcome the software and trust deficits left by previous attempts to challenge Nvidia's CUDA ecosystem. Intel's Gaudi 3 accelerator failed to gain traction, with the company recording inventory-related charges in 2024 and 2025 (https://startupfortune.com/intel-is-preparing-a-new-ai-chip-to-challenge-nvidia-this-year/). Nvidia's network effects are the deepest moat in AI infrastructure, and every inference-silicon startup must answer the question of whether buyers will recompile their model stacks for a non-CUDA runtime. The timing is unforgiving: by late 2026, Nvidia's Blackwell systems will be deeply embedded across hyperscaler fleets. The opportunity for inference-optimized silicon is real but narrow — winning workloads that can be moved without pain from Nvidia's platform, not displacing it in flagship deployments.

The Google-SpaceX deal crystallizes what these structural shifts mean in practice. Even the world's largest single owner of AI compute must rent from an emerging compute aggregator to bridge near-term GPU shortfalls (https://techcrunch.com/2026/06/05/google-will-pay-spacex-920m-per-month-for-compute/). Alphabet has already committed over $180 billion in capital expenditures this year and announced an $80 billion equity sale (https://techcrunch.com/2026/06/05/google-will-pay-spacex-920m-per-month-for-compute/). The cancellation clause after 90 days' notice following December 31, 2026, suggests this is a tactical bridge rather than a strategic realignment, but it nevertheless underscores how AI compute market dynamics now govern product roadmaps. Google explicitly attributes the deal to unexpected demand for its Gemini Enterprise agent platform, meaning demand-pull is overwhelming even Google's prodigious internal supply (https://techcrunch.com/2026/06/05/google-will-pay-spacex-920m-per-month-for-compute/). This suggests that enterprise agent platforms may be hitting a hockey-stick inflection point, and that the compute substratum — not model quality — is the near-term ceiling.

SpaceX itself is going public at a $1.77 trillion valuation, exceeding Tesla's roughly $1.6 trillion market cap, with the IPO filing disclosing that proceeds will fund Starship, Starlink, and AI computing tied to its integration with xAI (https://platum.kr/archives/288337). At 94.8x trailing 12-month revenue, the valuation reflects a capital-compression arc in which frontier-technology companies raise at institutional-scale valuations well before profitability. SpaceX swung from $791 million net income in 2024 to a $4.94 billion net loss in 2025 on $18.67 billion revenue (https://platum.kr/archives/288337). The IPO structure — a single fixed price before the roadshow, with retail investors granted direct access on day one — signals how capital markets are adapting to the scale and urgency of the AI buildout.

The key unresolved question is whether inference silicon will fragment around specialized architectures or consolidate around Nvidia's CUDA ecosystem as it did for training. Intel's cost-optimized LPDDR5X path, Qualcomm's ARM-based agentic inference play, and XCENA's in-memory compute thesis each represent a bet that the inference workload is structurally different enough to support a new silicon architecture — but each must also prove that the software ecosystem can follow. The OpenShell runtime on NVIDIA's DGX Station, with its sandboxed agent security model and Microsoft enterprise-management integration, suggests Nvidia is already preemptively extending its platform lock-in to the desktop agent environment (https://ascii.jp/elem/000/004/407/4407314/). The Run:ai acquisition pattern from the internal frame — where GPU orchestration was absorbed into CUDA — is a warning that standalone infrastructure layers with neutral APIs become acquisition targets for the dominant platform.

What is clear is that the inference inflection is not a future event. It is this week's news, embedded in a $920 million monthly compute lease, a $15 billion inference-platform valuation, a $30 billion Indian data center commitment, and six tents in Ohio. The industry is re-architecting in real time, and the companies that treat inference as the primary compute workload — not a residual to training — are the ones capturing the capital and the customers.

Notes. This week's reporting contains no direct evidence of a downside scenario in which inference demand plateaued or enterprise adoption slowed. The risk factors are structural rather than demand-driven: the $15 billion Fireworks valuation depends on sustaining ARR growth above 400% year-over-year, which becomes harder as the base expands; the Google-SpaceX deal's 90-day cancellation clause after December 2026 leaves the compute bridge exposed to any slowdown in Gemini Enterprise uptake; and Intel's Gaudi failure is a standing reminder that the distance between a credible inference chip announcement and enterprise deployment is measured in trust, not just performance specs. Each of these is a recognizable pattern from the internal frame's skeptic-memory layer, but none has yet manifested as a material event.