The Inference Silicon Race: Beyond GPUs

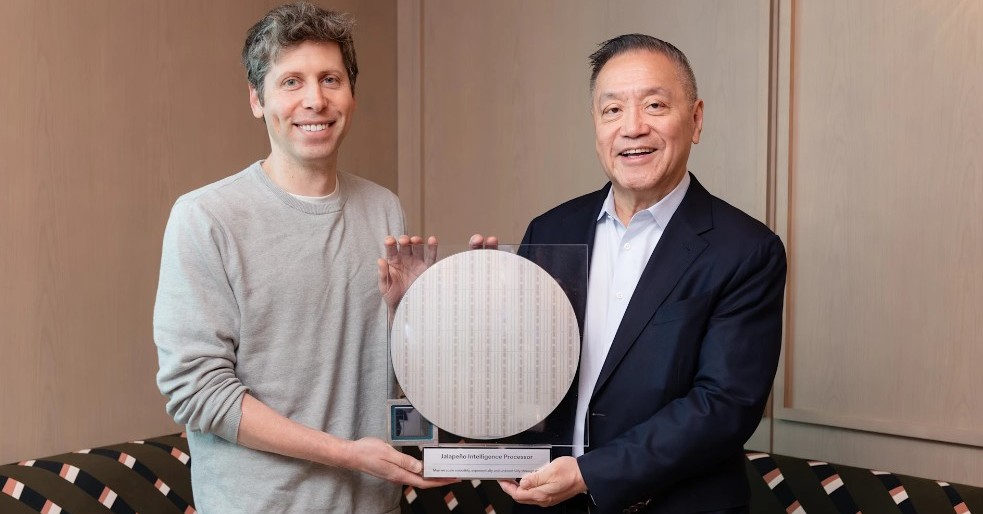

OpenAI and Broadcom's Jalapeno chip, designed and manufactured in nine months, is already running production inference workloads for GPT-5.3-Codex-Spark. That compressed timeline — roughly half the typical 18-to-24-month custom chip cycle — is the first signal that the inference silicon market is accelerating faster than most analysts anticipated.

The broader pattern is unmistakable. Etched announced that TSMC has manufactured its chip and booked $1 billion in contract orders, with an unannounced $500 million round closed at a $5 billion valuation (Etched hits $5B valuation). SambaNova Systems is poised to quintuple its valuation to $10 billion amid surging demand for Nvidia alternatives. UnconventionalAI, founded by former Databricks AI head Naveen Rao, raised $475 million in seed funding at a $4.5 billion valuation for an oscillator-based architecture claiming 1,000x power reduction — though the claim rests on software simulation alone (UnconventionalAI unveils oscillator-based architecture). A JD.com spinout raised hundreds of millions of RMB in angel funding for inference chips, following the same incubation-then-spinout pattern Baidu and Alibaba established.

What changed? For the first time in this cycle, multiple credible inference-only silicon efforts have crossed from design into manufacturing, with concrete revenue commitments attached. That shifts the debate from theoretical efficiency gains to actual market competition.

Evidence: Manufacturing Milestones and Customer Commitments

The Etched milestone is the most concretely grounded. The company's chip achieved first-pass silicon success on TSMC's N4P process, and its first rack-scale product is being validated with customers (Etched chip manufacturing details). The $1 billion in signed contracts — while customer names remain undisclosed, consistent with enterprise confidentiality — represents pre-revenue orders for full-stack inference systems. The investor syndicate, including Jane Street, Hudson River Trading, and Two Sigma alongside AI luminaries Andrej Karpathy, Geoffrey Hinton, and Fei-Fei Li, signals conviction from both quantitative finance and frontier AI research.

OpenAI's Jalapeno chip provides a different kind of validation: deployment at scale by a leading model lab. The chip targets roughly 50% lower inference cost per token compared to typical AI GPUs when running OpenAI's specific models, with an estimated cost per million tokens around $0.135 versus approximately $0.27 for an H100 on-demand (Jalapeno cost comparison). That 50% improvement, while significant, is incremental rather than a breakthrough — suggesting OpenAI is optimizing for economic margin on its own API traffic rather than seeking a dramatic efficiency improvement (OpenAI's Jalapeno chip details).

SambaNova's valuation jump to $10 billion reflects a different thesis: that reconfigurable dataflow architecture can capture inference workloads across a broader set of customers and models than custom ASICs. Its Intel backing and existing enterprise deployments position it as a second-tier silicon contender approaching decacorn status, though it still faces the hyperscaler distribution moat Nvidia has built through CUDA ecosystem lock-in.

Mechanism: The Post-GPU Compute Substrate

The technical divergence among inference silicon approaches is widening. At one end of the spectrum sit custom ASICs like Jalapeno and Etched's chip — application-specific integrated circuits hardwired for transformer inference, offering the highest efficiency for a narrow workload. At the other end sit radical architectural experiments like UnconventionalAI's oscillator-based system, which claims to replace transistor-based logic entirely with vibrating components that synchronize naturally to perform computations.

Between these poles sits SambaNova's reconfigurable dataflow architecture, which can adapt to different model architectures without the full generality (and overhead) of a GPU. And in China, the JD.com spinout joins Kunlunxin, Cambricon, and a wave of startups targeting domestic inference demand, driven by both geopolitical necessity and the shift from training-centric workloads to inference-heavy agent deployment.

The question is which architecture — or which combination — can achieve the R&D and manufacturing economies that give Nvidia its hyperscaler distribution moat. Nvidia's advantage is not primarily technical; it is structural. The CUDA ecosystem locks in software dependencies, the cloud partner program controls GPU allocation, and the sheer volume of H100/H200/B200 production amortizes fab costs across an unmatched unit base. Custom inference chips must overcome this installed-base inertia, not just the raw performance gap.

Precedent: Capital-Structure and Software Moats in Compute

The CoreWeave trajectory provides the closest analogy for what Etched and SambaNova are attempting (CoreWeave as precedent). CoreWeave's $19 billion revenue backlog, secured through multi-year take-or-pay contracts with Microsoft, OpenAI, and Anthropic, demonstrated that long-duration tenant commitments could underwrite debt-financed GPU build-outs. The company's commodity-finance founding team treated GPUs as depreciable long-duration assets — a capital-structure insight, not a technology insight.

Etched's $1 billion in pre-revenue orders follows a similar logic: customers are making forward commitments to inference capacity, betting that specialized silicon will deliver better unit economics than GPUs over the contract term (Etched contract orders). The difference is that Etched must manufacture chips at scale — a higher-risk proposition than CoreWeave's model of buying and deploying Nvidia GPUs.

Together AI's trajectory offers a different precedent: the neo-cloud with academic pedigree, combining compute with software differentiation through FlashAttention-lineage kernels and fine-tune platforms. SambaNova's reconfigurable architecture attempts a similar combination — unique hardware plus a software abstraction layer — but faces the additional challenge of convincing developers to target its architecture rather than CUDA.

Counter-Signal: The Unvalidated Claims

The most significant risk to the inference-silicon thesis is the gap between extraordinary performance claims and validated benchmarks. UnconventionalAI's 1,000x power reduction claim rests entirely on software simulation of 1,024 to 16,384 virtual oscillators; the company plans to release physical chip schematics shortly, but no silicon exists (UnconventionalAI validation status). The $4.5 billion seed valuation reflects option-value on a technology transition that has not yet demonstrated a working chip, not de-risked engineering (UnconventionalAI valuation).

Similarly, no publicly available benchmark compares Jalapeno's inference cost per token directly to Nvidia H100 hardware, because the chip is a proprietary ASIC not sold or benchmarked for external users (Jalapeno benchmark absence). The 50% cost reduction estimate comes from OpenAI's internal claims, not independent validation (OpenAI internal claim).

Etched's $1 billion in contract orders is the most substantiated claim — TSMC has manufactured the chip, and production systems are running at a customer site with models including DeepSeek, Qwen, Mamba, and Llama — but customer names remain undisclosed, and the stated path to gigawatt-scale deployment by 2027 is aspirational rather than contracted (Etched contract substantiation).

Implication: Fragmentation and the Supply-Chain Reshaping

If even half of these efforts deliver on their promises, the inference silicon market will fragment in ways that reshape supply-chain power. Custom ASICs will capture the highest-volume, most standardized inference workloads — OpenAI's API traffic, large-scale enterprise deployments, and hyperscaler internal inference demand. Reconfigurable architectures will occupy the middle ground, where workload diversity demands flexibility but the GPU's generality is overkill. Radical architectures, if they reach silicon and validate their efficiency claims, could open entirely new deployment paradigms at the edge or in power-constrained environments.

For Nvidia, the threat is not that any single competitor matches its absolute performance, but that the aggregate custom-silicon market erodes its pricing power and allocation control. If OpenAI cuts its inference costs by 50% through custom silicon, it can either compress API pricing to undercut competitors or expand margins to fund more R&D (OpenAI cost reduction impact).

For hyperscalers, the implication is more nuanced. Google already has TPUs. Amazon has Trainium and Inferentia. Microsoft is investing in both custom silicon and neo-cloud capacity. The inference silicon race accelerates each hyperscaler's vertical integration strategy, reducing dependence on Nvidia while increasing capital expenditure on custom chip design and manufacturing.

For startups and enterprises deploying AI, fragmentation means more choice in inference hardware — but also more complexity in deciding which architecture to optimize for. The first-mover advantage will accrue to platforms that abstract the hardware layer cleanly enough to let models run across custom ASICs, reconfigurable architectures, and GPUs without rewrites.

The nine-month design cycle of Jalapeno is the headline data point, but the structural shift is this: inference silicon has moved from the whiteboard to the fab, with real customer money on the table. The next twelve months will determine whether that money was well spent or whether Nvidia's generational lead in manufacturing economics and software lock-in proves durable.

Notes. No specific downside risk surfaced in this week's reporting regarding the JD.com spinout's technical milestones or customer pipeline — the event is too early-stage for validated benchmarks. That absence is itself a signal: the Chinese inference chip market remains pre-competitive, with capital flowing to teams on thesis rather than proof.